Cape Cod Real Estate Market Update: December 2025

The Cape Real Estate Market is poised to close out 2025 essentially flat over 2024. Median sale price is up 3.1% year-to-date. Though this is lower than we have been used to since the start of the COVID market era, it nonetheless represents healthy annual appreciation. At the same time, days on market continues to climb, currently registering at 27.3% higher than last year. Similarly, the percent of list price received by sellers continues to decline to 95.5% - only .1% higher than the post-COVID low reached in February of this year. In plain English, homes are selling more slowly for less than asking price, but on average for slightly more than they were in 2024. A decidedly mixed message.

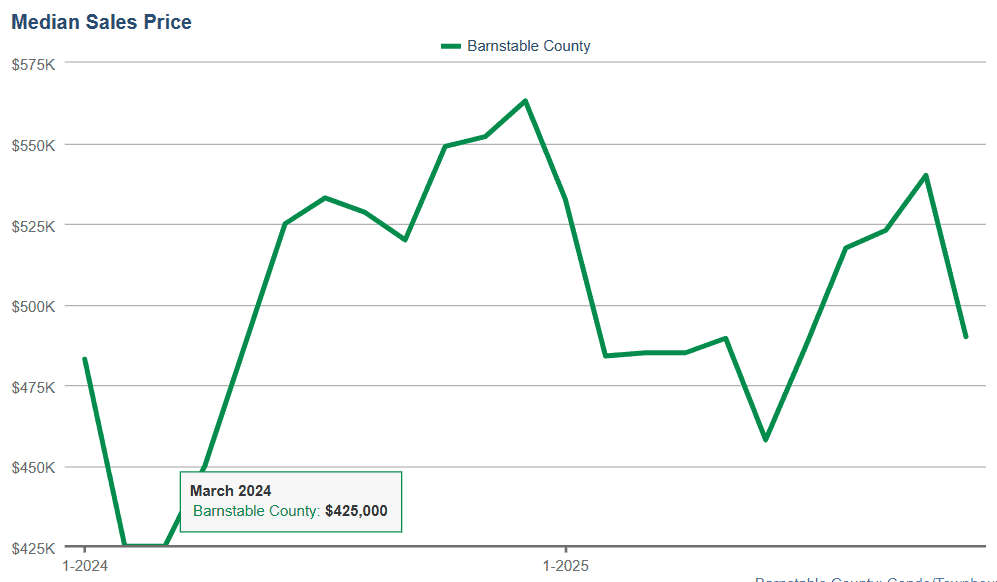

The message becomes even more mixed if you compare single family home performance against condominium properties. The accomanying graph (released this month by the CCIAOR) shows the median price of condominiums only. As you can see, declines in condo prices have consolidated over the last few months. Condos are in fact on track to close the year down at least 4.9%. Historically condo prices have been a leading indicator for changes in the overall real estate market. We will continue to monitor these trends...stay tuned for more in the New Year.

And whether you own or want to own a condo or single family home...whether you are planning a vacation here or want to list your home for rent...the professionals at Chatelain Real Estate are here to give you the expert advice you will need to make your transaction a success. Give us a call any time - we look forward to hearing from you.